How to Calculate Monthly Payments on a Loan

Understanding how to calculate monthly loan payments can be highly beneficial and crucial when dealing with loans. When you get approved for a loan, your lender will furnish you with repayment details, specifying the amount and schedule. However, knowing how to perform these calculations can provide valuable insights when comparing loan options and deciding on the most suitable one for your needs.

By grasping the methodology for calculating potential monthly loan payments, you gain a powerful tool while shopping around or researching loans. This allows you to comprehend the actual costs associated with different loans, aiding in effective comparisons.

Additionally, having this knowledge empowers you to make informed decisions about the feasibility of a specific loan type. For instance, if your budget only permits a $200 monthly payment, and after performing calculations, you find that the estimated monthly payment for a loan is $300, you can determine that the loan is not viable for you at this moment.

Here’s a step-by-step guide to help you calculate a rough estimate of monthly loan payments. A simple calculator on your computer or smartphone should suffice for the required mathematical computations.

Step 1: Familiarize Yourself with Loan Types

The formula for computing loan payments can vary based on the type of loan you are dealing with. Two common loan types are amortized loans and interest-only loans.

An amortized loan involves paying more interest and less principal during the initial stages of repayment. As time progresses, a larger portion of your monthly payments goes towards reducing the principal, with less going towards interest. This type of loan is typical for car and home loans.

On the other hand, an interest-only loan requires you to make payments solely towards the interest initially. The principal amount borrowed only starts getting repaid after the interest is fully settled.

For the purpose of this guide, we will focus on calculating payments for amortized loans.

Step 2: Understand the Terminology

To calculate monthly loan payments, you will need three essential pieces of information:

- The total amount borrowed (a).

- The interest rate is expressed as a decimal and divided by 12 (to represent months in a year) (r).

- The total number of months over which you will make loan payments (n).

At times, you may not have all of this information readily available. For instance, you might know that you need to borrow $5,000 and aim to pay it back within 3 years. In such cases, you will need to conduct further research to identify the interest rates offered by various lenders to estimate a monthly payment.

Step 3: Utilize the Formula and Perform the Calculation

Once you have gathered all the necessary information, it’s time to apply the formula:

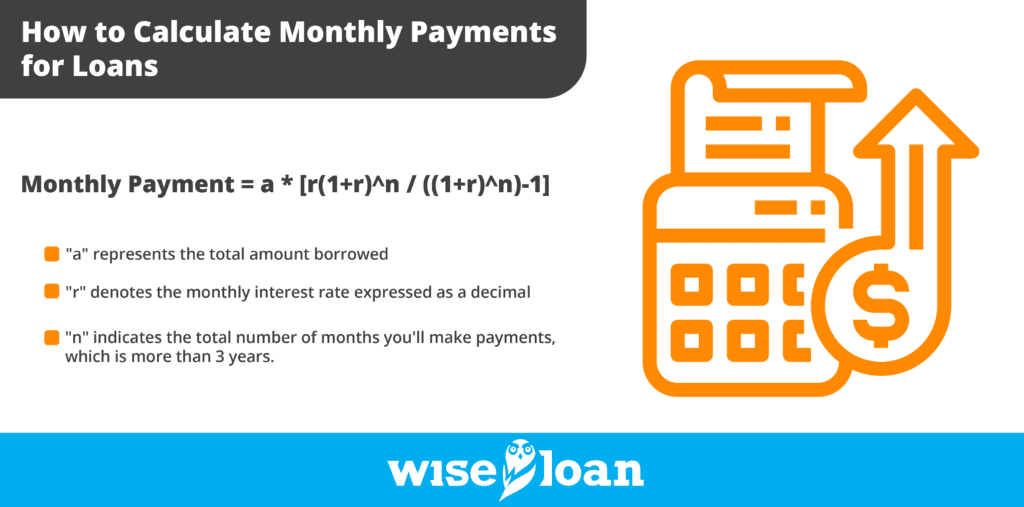

Monthly Payment = a * [r(1+r)^n / ((1+r)^n)-1]

In this formula:

– “a” represents the total amount borrowed, which in this case is $5,000.

– “r” denotes the monthly interest rate expressed as a decimal. To get this value, divide the annual percentage rate by 100 and then by 12. For this example, it would be 0.0075.

– “n” indicates the total number of months you’ll make payments, which is more than 3 years. You can calculate it by multiplying 3 years by 12 months, resulting in 36 months.

Let’s walk through a hypothetical example to clarify the process:

Starting with the middle of the formula: r(1+r)^n. Plugging in the numbers, the calculation looks like this:

0.0075 * (1 + 0.0075)^36

0.0075 * 1.309

0.0098

Next, proceed with the last part of the formula: [(1+r)^n]-1. With the given values, the calculation is as follows:

(1 + 0.0075)^36 – 1

(1.0075)^36 – 1

1.309 – 1

0.309

Now, combine the results and insert them into the formula: a * [(1+r)^n – 1] / (r(1+r)^n).

Therefore, the calculation becomes:

$5,000 * (0.0098 / 0.309)

$5,000 * 0.0317

The estimated monthly payment is $158.50.

An Easier Approach to Calculate Monthly Loan Payments

While the above method provides a precise estimate, it involves complex calculations and leaves room for errors. If dealing with such arithmetic operations seems daunting or time-consuming, don’t worry. There’s a simpler way to determine monthly loan payments.

Numerous online loan calculators are available to handle the math for you. By inputting the interest rate, loan amount, and repayment duration, these tools can swiftly provide accurate results. Just ensure that the online loan calculator you use is suitable for the specific loan type and interest rate you’re exploring. With these user-friendly tools, you can obtain your estimate within seconds.

Reducing Your Monthly Loan Payments

If you aim to minimize your monthly loan payment, consider these approaches:

- Extend the Loan Term: Opt for a longer repayment period. The more months you have to pay back the loan, the smaller the monthly installments will be.

- Borrow Less: Request a smaller loan amount. By borrowing less over the same duration, your monthly repayment amount decreases accordingly.

- Secure a Better Interest Rate: A lower interest rate will result in a less expensive overall loan and subsequently reduce your monthly payment burden. If you have good credit, explore various lenders to find more favorable interest rates. In case your credit score needs improvement, consider taking steps to enhance it before applying for a loan, especially a significant one.

At Wise Loan, we provide loans that help you build credit while offering the financial support you need. Approval does not solely depend on good credit, and we report your timely payments to two of the three credit bureaus, helping you improve your credit score. Consider applying today for a loan that supports your goals.

The recommendations contained in this article are designed for informational purposes only. Essential Lending DBA Wise Loan does not guarantee the accuracy of the information provided in this article; is not responsible for any errors, omissions, or misrepresentations; and is not responsible for the consequences of any decisions or actions taken as a result of the information provided above.

More information on Installment Loans and how they work in your state: